Introduction

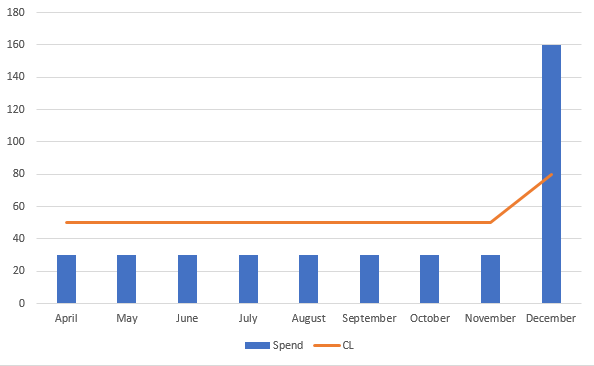

An infamous reader of mine, who has been shut down before from another bank, told me his wife’s Chase account was shut down recently. It was pretty easy to see why he was shut down. In his defense, he had paid off the $160K spend before the statement closed, but the train already left the station for this Chase shutdown story.

AMEX Charge cards

He also thinks another factor is the AMEX personal charge cards. I remember when I was refinancing my mortgage , my broker asked me why my minimum amount due on my AMEX charge card was the balance amount. At the time, I didn’t think anything of it and told her that’s how AMEX charge cards work. Now I wonder if AMEX charge card balances = CL on his CR. So if your AMEX charge card closes at $5K, if your reported CL is also $5K. Or maybe they don’t report a CL; let’s say you have 2 credit cards on your CL – one has a $1K balance out of $10K CL and your AMEX charge card has a $9K balance, I wonder if the sum would equal $10K balance on a $10K CL. Worst case, you have a 100% utilization; best case, you have a 53% utilization. Either way, these AMEX charge cards are bad for your utilization.

Lessons Learned

A ramp up in spend, in this day and age with Chase or any other bank, seems to be a huge red flag. Also try to pay off your AMEX charge cards before the statement closes.

Note that the “ramp up in spend” was spending $160,000 in one month on a credit card. Of course that’s going to draw a red flag.

Amex charge cards haven’t reported that way in years. Nowadays they are completely excluded from util calcs. Please don’t spread misinformation.

Vinh, you say at the end, ” Also try to pay off your AMEX charge cards before the statement closes.”

Do you mean before the DYUE DATE, or literally before the cycle closes? I usually pay as soon as I get the email that it is ready but should I move even faster and try to beat the billing cycle?

He means before the statement close date so that it prints at $0 and doesn’t use any of your utilization.

Paying (even in full) by due date does nothing to reduce utilization. Whatever the balance is gets reported to bureaus.

As a mortgage underwriter, yes, please pay Amex charge cards before statement cuts! Problem with that is it shows as either a $0 payment or full balance payment. Either way, normally needs a little attention and possibly follow up docs from borrower. As it relates to this, however, I don’t think it’s the high utilization but rather the past high limit previously reported might be an issue. With trending data now being reported, some credit reports will see balances over time and I bet Chase doesn’t like seeing those jump all over the board. Probably see that as a high risk.

Sheeesh!!! I think anyone could have projected this shutdown!

Unless you make 7 figures, I would have shut down that personal account too.