For the past month or so, I’ve been seriously looking at my retirement funds and when the time to retire should be (that’s for another post.) That’s when I decided to look for a good resource to track my retirement savings as well as my wife’s. I had given up on Mint a long time ago due to all the MS charges skewing the real data. I have accounts from 3 sites, and I’ve been sorta guesstimating our total savings, but I was happily surprised when I saw the 3 total amounts all in one place. Here’s my quick review of Personal Capital and Sigfig.

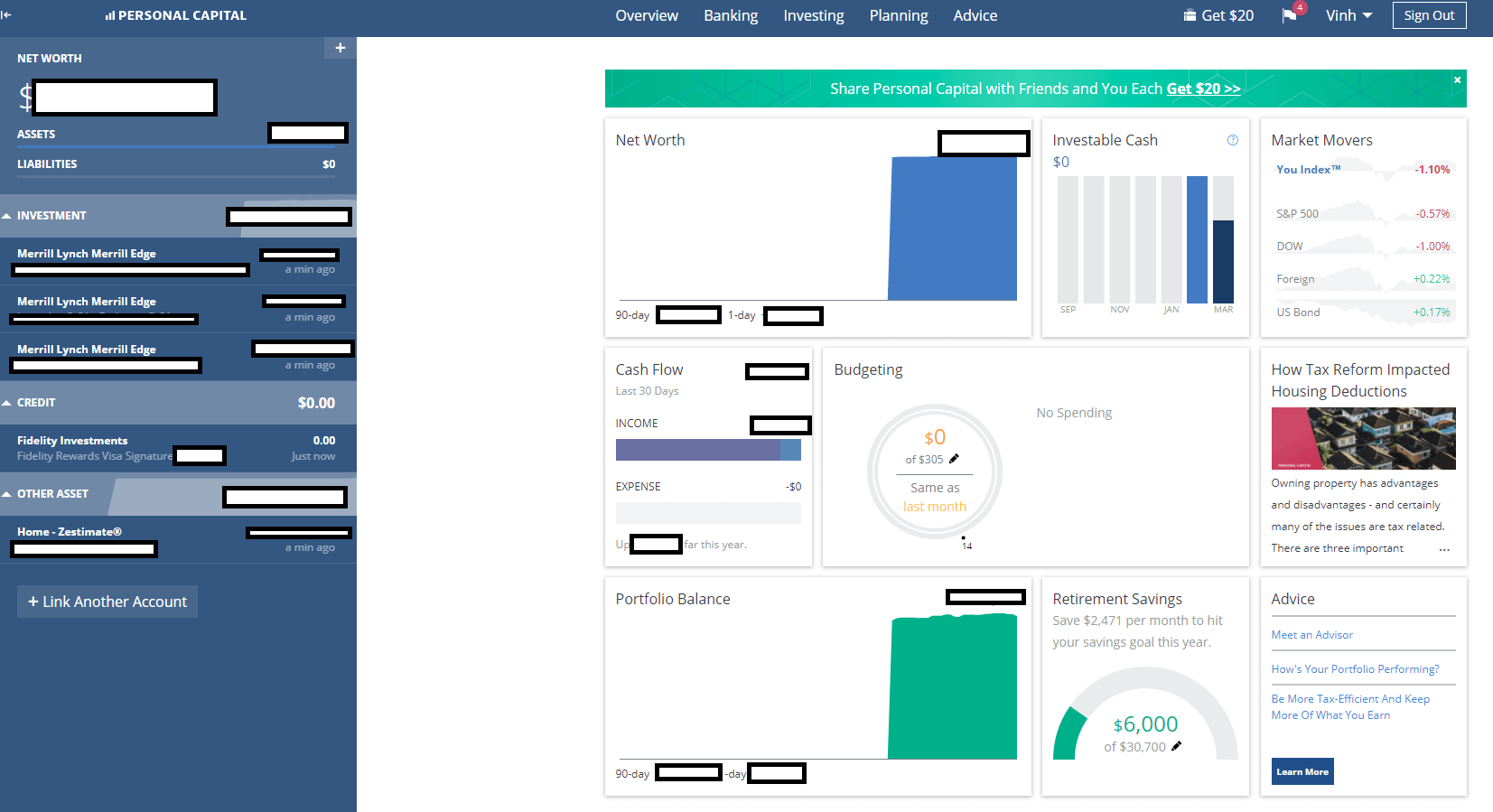

Personal Capital

I liked the pretty charts and the ability to add my house as a Zestimate. However, I didn’t like the phone call a week later from a guy trying to sell me on their services. I also had an issue trying to add both my and my wife’s Fidelity accounts. That was a deal breaker. I stopped using it after that.

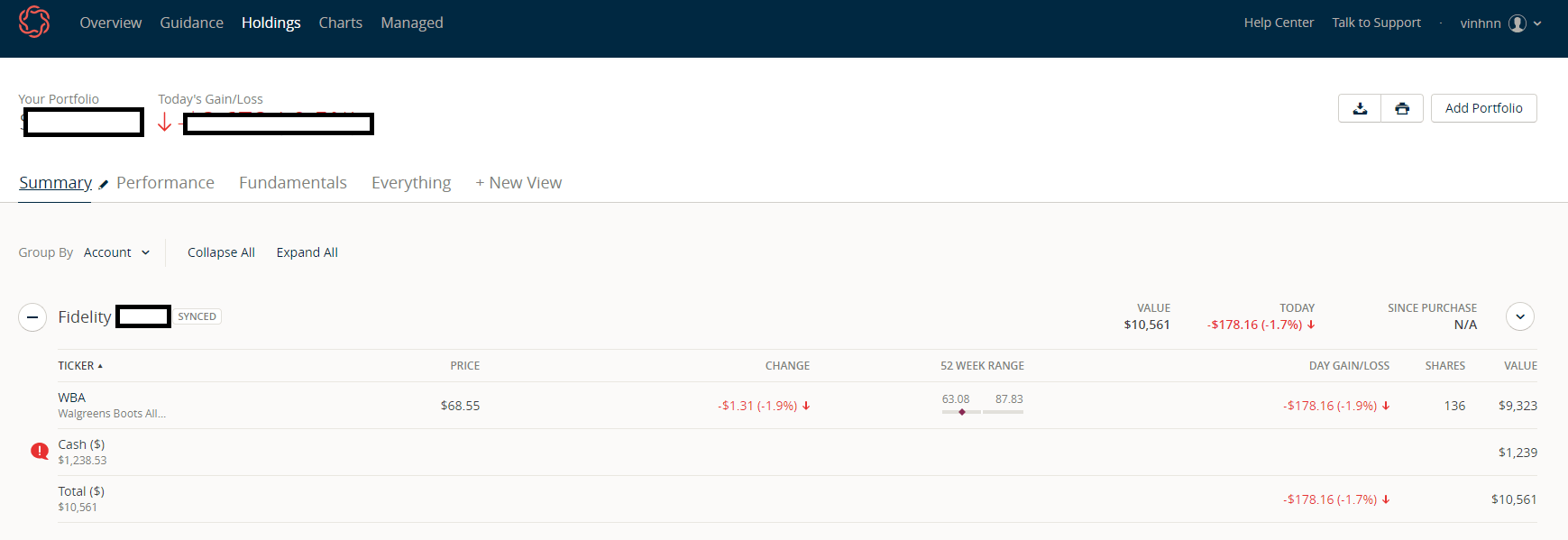

Sigfig

When you create an account, there comes a point where you want to abandon the set up and just add your accounts. That’s the only gotcha. Once you have everything set up, you can see it’s pretty “plain.” No pretty charts; just numbers.

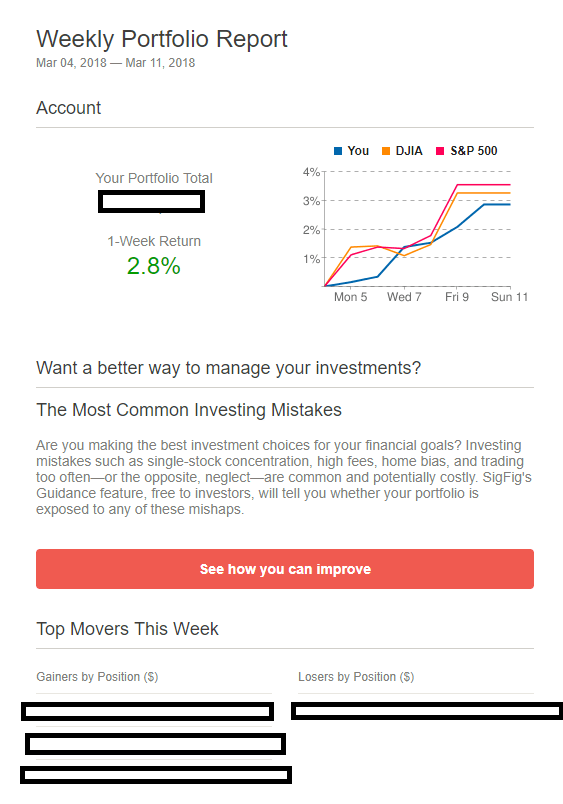

Weekly Emails

What ultimately made me decide on Sigfig is their weekly email recap. On personal Capital, it just says, “You’re portfolio is up 1% this week.” It doesn’t drill down into individual stocks or anything. Half the email is an ad for an article. Sigfig’s weekly email is better. It gives me the same portfolio increase and also gives me my 3 best and worst stocks.

Conclusion

If you’ve been looking for a site to consolidate all of your retirement accounts, I’d reco you go with Sigfig for their weekly email recap as well as lack of someone calling you and trying to upsell you on investment advice.

Will look into this…thanks, Vinh.

I signed up with personal capital. They said they’d help with not just investing, but 529s, etc. They had a very competent advisor and he was our contact… Until they had the funds. Then we got his assistant. And that person had no knowledge about markets or retirement vehicles and especially no knowledge of educational funds. When my attempts to get back to the main person failed, we canceled and left. Then, all of a sudden he was back and so was his boss. Too little, too late.

Like the finance posts. Thanks Vinh